Love your future. Shell Pension.

Love your future. Shell Pension.

November 2020

Main financial risks

The main financial risks for SSPF are: interest rates, market, inflation and longevity risk.

Interest rate risk is the possible impact of changes in the interest rate curve prescribed by the DNB on the value of the investments and the liabilities. A fall in the interest rate leads to an increase of future liabilities. This is because a fall in the interest rate means that lower interest income is to be expected in the future and, as a result, more money needs to be kept in the bank to pay the same pension obligations. An increase in the interest rate has the opposite effect. The fund has a dynamic interest rate hedging policy based on the Solvency Risk Budget.

Market risk

Investing (amongst others in shares and alternative investments, such as hedge funds, private equity and real estate) entails market risk. These are limited by spreading the risks as widely as possible (diversifying) across countries and regions, sectors and specific investments therein.

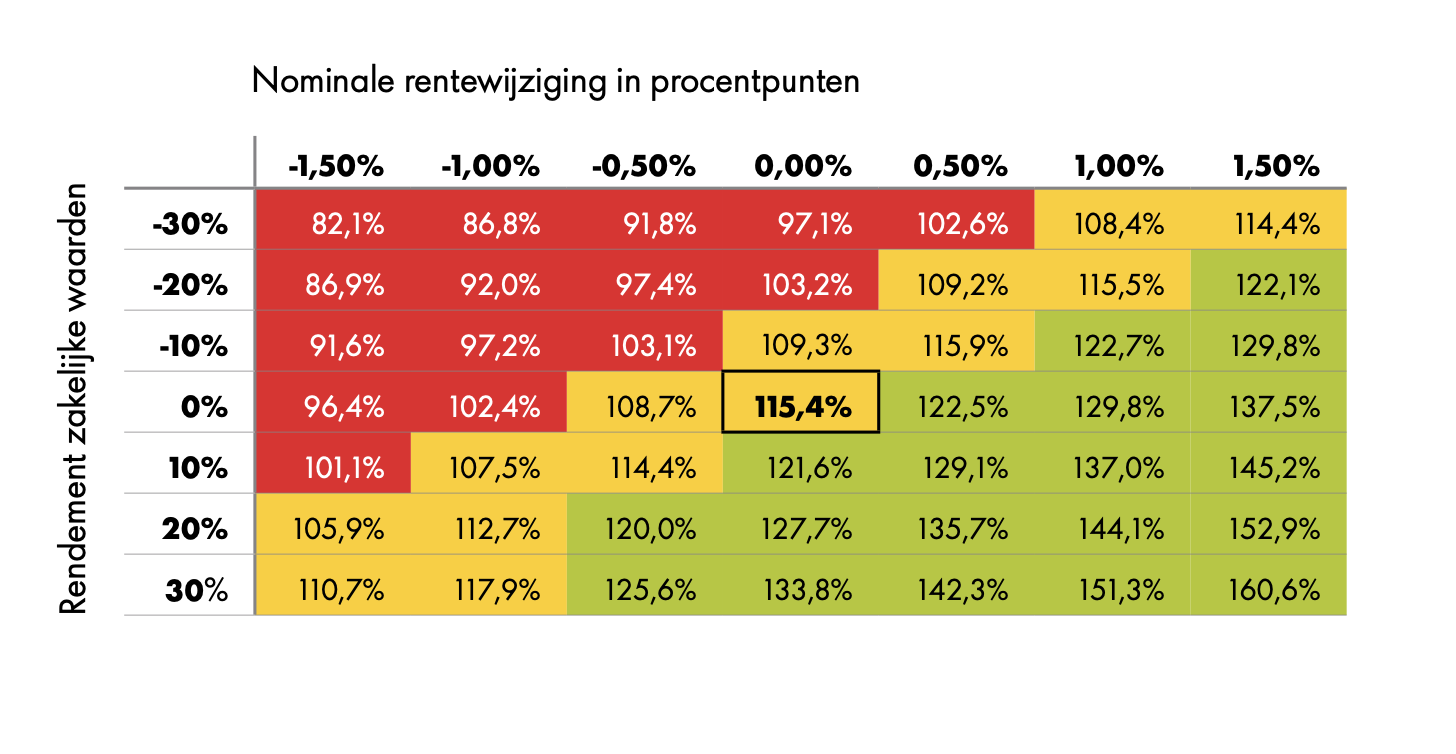

The table below shows the impact on the funding level of changes in the nominal interest rates and the return on marketable securities at yearend 2020. Quite striking is the substantial difference in impact between changes in interest rates and returns.

Inflation risk is the risk that the fund cannot meet its indexation ambition due to inflation. Practically, this means the risk that we won't be able to sufficiently compensate for a rise in price levels with our investment results which means that no or only partial indexation can take place. The board has decided that partial hedging of this risk should be considered at higher coverage ratio levels. At lower coverage ratio levels the policy emphasis is on protecting those pensions that have to be paid out.

Longevity risk is the 'risk' that participants will live longer than assumed when the pension liabilities provision was determined. In other words, the required pension capital is higher than originally estimated. The increased life expectancy in recent years has therefore had a negative impact on our coverage ratio. When estimating the provision, the fund uses the latest prognosis tables of the Actuarial Association and the fund-specific experience mortality rate.